This blog complements our YouTube video, where we analyzed an INC.com Article.

We scrutinized several sections in the article, The SBA Will Keep Its Covid Loan Portfolio to Avoid Taking a $120 Billion Haircut by bringing a unique perspective thanks to our 30-year-plus loan officer who specialized in government loans, has worked on several hundred EIDL files, has had thousands of interactions with business owners and SBA reps on EIDL files, transactions, business changes, etc.

Thank you, Inc.com, for writing this article. Previously, the only media attention on this U.S. Treasury debacle, which has been going on for several months, was an article in the Wall Street Journal.

We think Inc.com did a credible job discussing these elements, giving us an opportunity to illuminate them point-by-point and provide more depth so that you can understand the program.

Why We Spoke Up About This Article

We started working on COVID-19 EIDL applications in March and April 2020. We helped our clients get an estimated $70 million in approved loans.

We estimate that, with the free videos on our YouTube channel and various blogs on our website, including how-to instructional videos and live Q&A sessions, we helped small business owners get approved for another $30 million on their own.

The Implications of this Article

Inc.com specifically addressed the COVID-19 EIDL program and how, under tremendous political pressure from certain politicians in Washington, D.C., the SBA was going to take a huge tranche of the COVID-19 EIDL portfolio and sell to private collection agencies. We’ll address why that’s bad for business owners.

The other element of our conversation about the article, based on our expertise and day-to-day interactions with SBA, is that we have a different understanding of the statements made in this article. We’ve outlined those statements to give insight to help you arrive at an action plan that you will want to implement. It has to do with you and the political representatives who represent you.

Consequences for Business Owners

If you have recently suffered the terrific trauma of having your COVID-19 EIDL shipped off to the Treasury for collection by the SBA due to their systemic failures under the program, you want to review this blog and watch our video.

If you haven’t yet entered repayment because your 30-month deferment period hasn’t ended yet, you want to be aware of what’s going on behind the scenes to help you make decisions about how you’ll interact with SBA.

Even though the SBA has systemic failures, this does not relieve you of the responsibility to participate in resolving issues that occur with your EIDL. These issues will not be resolved on their own. You must participate in the process despite that SBA is the one that caused the issues in the first place.

Debate on Business Owner Responsibility

Linda Rey and Trevor have a long-standing disagreement about how much responsibility the business owner has regarding their EIDL despite SBA’s dysfunction.

We have been assisting small business owners who hired Aurora Consulting since January 2024 to help get their loans removed from collection activity at Treasury and returned to servicing at the SBA. Hearing their stories made Trevor more and more disgusted with the dysfunction of the SBA and its failures to help its constituents, the small business owners, properly understand the terms of the loan, understand the repayment procedures, and make payments on the loan.

Linda Rey’s perspective on this is that if you’re a business owner and have an EIDL, you’ve got to be aware of what’s happening with your loan. You need to understand the status of your EIDL, what requirements need to be tended to. Trevor pushes back often and says it’s not entirely their fault.

Linda Rey supports the basic tenet that business owners need to do a better job managing their loans, given the dysfunctional SBA.

Ill-preparedness and Excuses

Being busy is not an excuse. The first step needs to be catching yourself when you’re making an excuse. And catching yourself when you’re trying to say, this is not my fault, but isn’t it if you didn’t stay on top of the status of the loan while in SBA’s custody? You know you have this EIDL. You signed for it. It is your responsibility. And it’s your fault if you’re not following the procedures or at least being proactive, knowing the SBA is dysfunctional.

Article Analysis

In the first paragraph, Inc.com mentions how the SBA decided that it would not sell one of its “pandemic-era loan portfolios.” The Pandemic-Era Loan Portfolio is the COVID-19 EIDL program. This differs from the historical Natural Disaster EIDL program that’s been around since 1953. There’s a distinction between the two EIDL programs hence why it’s important that we clarify this term.

How Borrowers Can Default

The article claims that the COVID-19 EIDL program has an estimated default rate in the double digits. We’ll do some math later on, which will make you chuckle. Let’s talk about what does that mean. Let’s define default.

1. You’re not paying the loan back: Non-payment of the EIDL

However, you could also be in default if you engage in certain changes without notifying SBA or getting permission, such as:

2. Sold your business

3. Brought in an investor

4. Sold assets

We outline other scenarios in our SBA COVID-19 EIDL Guidebook.

In the case of EIDLs that were transferred to Treasury in late 2023, we believe it’s primarily due to default of non-payment.

But what does non-payment mean? Does it mean somebody who never made any payments and never intends to make payments?

It could mean that you’re 30 days late on your payment. By federal regulation, once you’ve reached 120 days of delinquency on payments, the SBA must automatically assign your loan for collection to the United States Treasury, which adds a 30 percent penalty. This means Treasury can garnish wages, W2 payroll, offset tax refunds, and other federal government payments.

it also means that Treasury could send your loan to a private collection agency.

SBA Communication Failures

We’ve seen folks who were attempting to make payments, but it wasn’t the full monthly amount per the loan agreement. This is where SBA failed at the Hardship Accommodation Program as a means to alleviate monthly payments while businesses were still recovering from the pandemic.

SBA never really made a formal announcement about HAP, even when folks were calling to figure out how to make a payment, even if it was less than the terms on the LAA. This is another reason we are relentless in urging you to be better than the SBA and have everything documented.

How You Can Default for Non-Payment

1. You never received a notification that your first payment was due

2. You received the notification, and the due date is unclear

3. Borrowers were/are confused about the end of their 30-month deferment period

Our estimate is approximately 1.2 million EIDLs are coming due between June and October of 2024.

Many business owners thought the deferment period started when their EIDL was approved for an increase. In fact, we’ve heard folks say, “Oh, I got my second loan.” The EIDL was one loan with an increase modification. However, we know SBA screwed this up, too, for some folks and issued a separate loan agreement in addition to the original 2020 EIDL approval.

Because of SBA’s poor training and communication, they didn’t teach people about this distinction of the program.

4. SBA’s changing technology issue

In 2022, if you wanted to pay your loan, you created an account on pay.gov. Then, in early 2023, SBA transitioned that to a new portal called Lending.MySBA.gov. And there was a whole host of problems with that.

5. ACH payments

People scheduled payments, but SBA did not access the account to transfer the funds to satisfy the payment requirement. Instead of notifying the borrower about a failed payment, they marked the file with a delinquent payment status and applied it to the next month with no notification.

6. Failure to roll out a more timely Hardship Accommodation Program

This gives you reduced payments for six-month periods. Not only did the SBA keep that a massive secret in early 2023, but they also managed it terribly. People would call and say, “I’m having difficulty making payments,” and the SBA representatives would not offer it to them to help them manage repaying the loan.

7. Relying on phone calls to the SBA

To this day, we tell people, whenever possible, not to call the SBA. You’re wasting your time and risk getting misinformation.

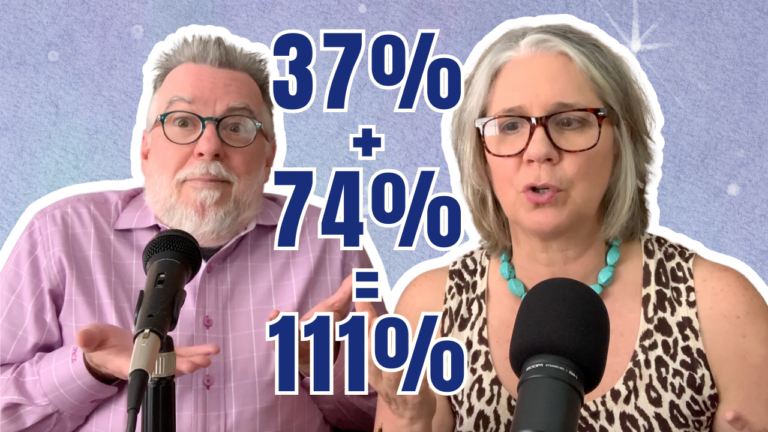

The Math Doesn’t Add Up

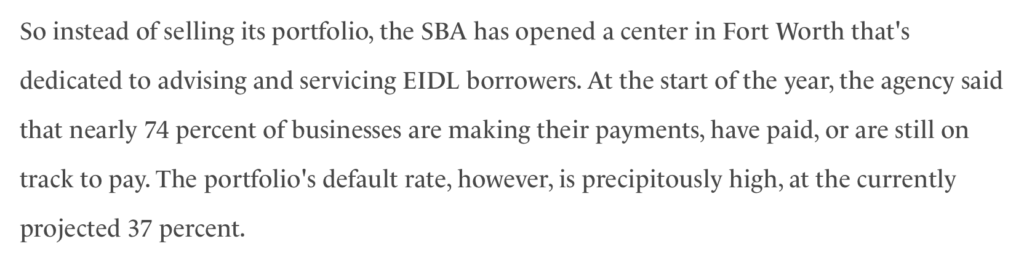

The article cites an estimated default rate of 37% of the EIDL portfolio. How can this agency calculate something that isn’t even functioning properly?

The article also cites that nearly 74% of businesses making their payments have paid or are still on track to pay. Then, how is it that there is a 37% default rate?

Another crucial factor to consider is the significant number of loans that have not yet entered full repayment. This is due to their 30-month deferment periods, which are only now ending between June and October of 2024.

Last year, between political pressure from politicians who don’t understand the program and do not support small business owners, the SBA’s Office of Inspector General would talk to any news reporter he could access, any politician he could get in front of, any congressional or senate committee he could talk to, and claimed that his Office of Inspector General, which is supposed to help the agency prevent fraud and prosecute criminal behavior, estimated massive fraud.

It was reported that they estimated half of the EIDLs were fraudulent. He claimed that 2 million out of the 4 million loans were fraudulent.

Political Pressure

In the article, it cited that Republican lawmakers have been calling for a sale of the portfolio. They put extra pressure on the SBA. We believe the politician’s soundbites are self-serving. Plus, it’s an election year.

If small businesses are the backbone of the economy, why is the SBA the most underfunded agency in government, given its monumental mission of managing the COVID-19 EIDL program AND the ongoing Natural Disaster EIDLs, and all the dysfunction behind that program and process?

In our humble opinion, the bottom line is that they have failed small businesses. Politicians don’t know small business. They are not small business owners. There may be a handful of politicians who are business owners, but for the most part, these career politicians are a joke.

Loan Portfolio Sale and Private Collectors

Selling the portfolio would require that anyone in the private market would demand a steep discount on the value of the portfolio. So that’s the “haircut” reference in the article.

The other element is that SBA is not completely ruling out that sometime in the future, they have the option to sell this portfolio off or a portion of it, and if that happens, it could be worse for small business owners than if the Treasury handles it. Why?

Suppose a private portfolio lender buys a section of this portfolio from the SBA. They’re going to come after business owners, fierce and fast for the debt because they want their money. If you’ve ever defaulted on credit card, car loan, or mortgage, and the lender sells that bad debt to a collection agency, they sell it to you with the haircut for pennies on the dollar. That means they are relentless in collecting.

Advocate for Better Support

We urge you to contact your political representatives to advocate for better SBA funding and support.

We provide templates in our SBA COVID-19 EIDL Guidebook.

While we’ve tried to peel back the layers of this article, the layers of bureaucratic mismanagement are many. We encourage taking proactive steps to ensure survival and success in these challenging economic times.

Knowing is half the battle; the other half is action.

For those seeking comprehensive guidance, our EIDL Guidebook is a treasure trove of information and instruction, offering step-by-step solutions for navigating this turbulent environment.